Carlos Madrid

New Member

Hi, i do not know if this has been reported, but default correlation formula in page 19 is confusing: square root of pi2(1-pi2) should not be squared 2 times.

regards

regards

Hi @David Harper CFA FRMHi David and Nicole,

here one more typo in the same reading De Laurentis, Chapter 3 "Ratings Assignment Methodologies" on page 21:

View attachment 1378 View attachment 1379

The cumulated normal disribution operator N is missing.

Thank you and kind regards!

"If the debt is risky, there is no guarantee the principal amount will be repaid in full. Specifically, if the value of the firm falls below the principal amount, if V(T) < F, then the firm is insolvent and the debt holders can only recover the firm's value. Therefore, the payoff to debt holders is Min[V(T), F]; i.e., their payoff must be at least equal to the firm's value but cannot be greater than the principal amount. Further, Min[V(T), F] = F - Max[F - V(T), 0], which illustrates that the debt holders' payoff is economically equivalent to the debt principal minus the payoff of a put option on the firm's assets, V(T), with an exercise price equal to K. Consider the same example where F = $100. If V(T) = $120, then debt holders receive Min(100, 120) = 100 - Max(100 - 120, 0) = $100. But if V(T) = $80, then debt holders receive Min(100, 80) = 100 - Max(100 - 80, 0) = $80."

@David Harper CFA FRMHi @David Harper CFA FRM

R44.P2.T6 Malz Study Notes page 42:

I think the Default01 formula should have 1/20 multiplied by the difference in the next 2 terms rather than just being 1/20th of the 1st term.

Current formula:

View attachment 1510

What I think it should be:

Default01 = 1/20 * [(mean value/loss for Pi + 0.0010) − (mean value/loss for Pi − 00.0010)]

Thanks

Karim

")

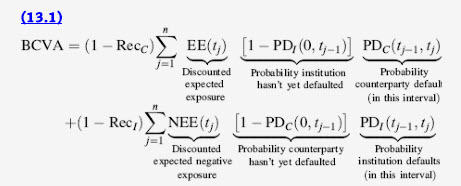

Hello @jaivipindefault correlation should be like below I believe..

View attachment 1800

if you please see it is like below in the doc.

View attachment 1801