gargi.adhikari

Active Member

Hi,

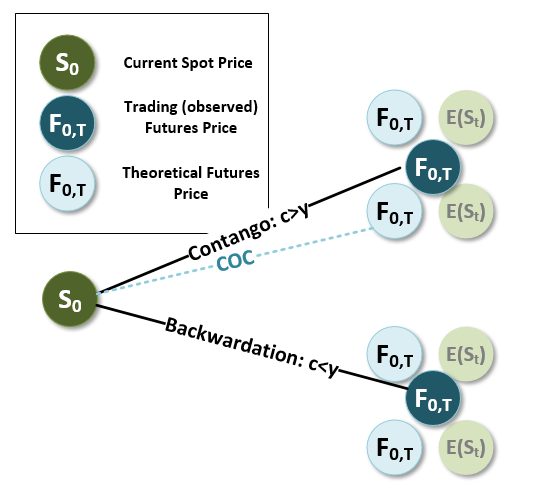

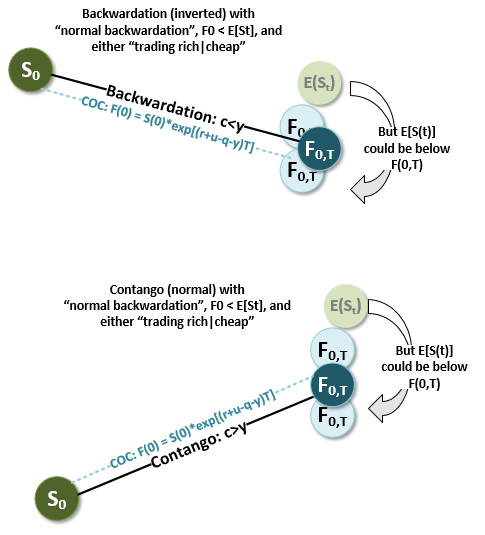

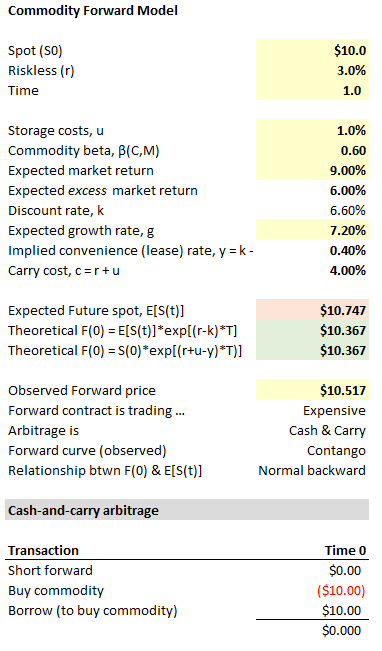

A Futures Contract is said to be Trading Rich when :

the Actual Price E(St) > the Model Predicted Price = F0=S0* EXP[ ( Rf + Storage Costs ) - ( Div + Yield ) ] T--> Normal Contango

A Short Futures Contract would Deliver as Late as possible when (Div + Yield ) > ( Rf + Storage Costs) and this happens when Futures Contract Price is decreasing with time-> Backwardation

Would it be correct to tie the "Trading Rich" condition to the "Delivery as Late as possible"

and the "Trading Cheap" condition to the "Delivery as Early as possible"

A Futures Contract is said to be Trading Rich when :

the Actual Price E(St) > the Model Predicted Price = F0=S0* EXP[ ( Rf + Storage Costs ) - ( Div + Yield ) ] T--> Normal Contango

A Short Futures Contract would Deliver as Late as possible when (Div + Yield ) > ( Rf + Storage Costs) and this happens when Futures Contract Price is decreasing with time-> Backwardation

Would it be correct to tie the "Trading Rich" condition to the "Delivery as Late as possible"

and the "Trading Cheap" condition to the "Delivery as Early as possible"

")