desh

New Member

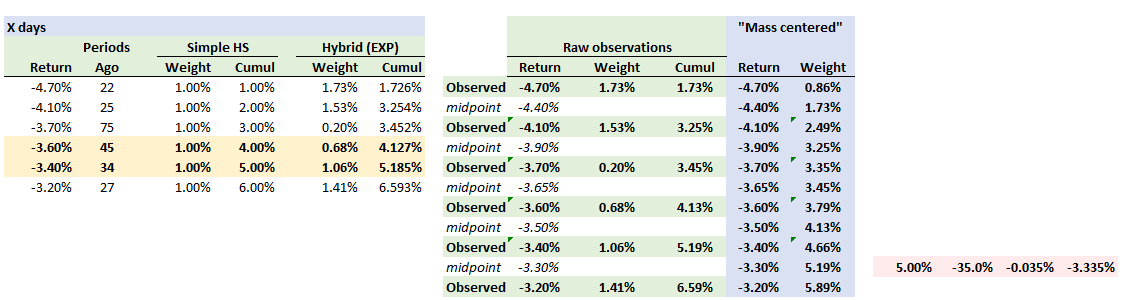

The 5th percentile should be between lowest and 2nd lowest transaction i.e. -4.70 % -4.10%

then how -3.6% and -3.4% choosen??

Please clarify

")

")

In contrast, the hybrid approach departs from the equally weighted HS approach. Examining first the initial period, table 2.3 shows that the cumulative weight of the −2.90 percent return is 4.47 percent and 5.11 percent for the −2.70 percent return. To obtain the 5 percent VaR for the initial period, we must interpolate as shown in figure 2.10. We obtain a cumulative weight of 4.79 percent for the −2.80 percent return. Thus, the 5th percentile VaR under the hybrid approach for the initial period lies somewhere between 2.70 percent and 2.80 percent. We define the required VaR level as a linearly interpolated return, where the distance to the two adjacent cumulative weights determines the return. In this case, for the initial period the 5 percent VaR under the hybrid approach is:

2.80% − (2.80% − 2.70%)*[(0.05 − 0.0479)/(0.0511 − 0.0479)]

= 2.73%.

Similarly, the hybrid approach estimate of the 5 percent VaR 25 days later can be found by interpolating between the −2.40 percent return (with a cumulative weight of 4.94 percent) and −2.35 percent (with a cumulative weight of 5.33 percent, interpolated from the values on table 2.3). Solving for the 5 percent VaR: 2.35% − (2.35% − 2.30%)*[(0.05 − 0.0494)/(0.0533− 0.0494)]

= 2.34%.

In contrast, the hybrid approach departs from the equally weighted HS approach. Examining first the initial period, table 2.3 shows that the cumulative weight of the −2.90 percent return is 4.47 percent and 5.11 percent for the −2.70 percent return. To obtain the 5 percent VaR for the initial period, we must interpolate as shown in figure 2.10. We obtain a cumulative weight of 4.79 percent for the −2.80 percent return and 5.11% for -2.60% (which is the midpoint between -2.70% and -2.50%). Thus, the 5th percentile VaR under the hybrid approach for the initial period lies somewhere between 2.60 percent and 2.70 percent. We define the required VaR level as a linearly interpolated return, where the distance to the two adjacent cumulative weights determines the return. In this case, for the initial period the 5 percent VaR under the hybrid approach is:

2.70% − (2.70% − 2.60%)*[(0.05 − 0.0479)/(0.0511 − 0.0479)]

= 2.63%.

Similarly, the hybrid approach estimate of the 5 percent VaR 25 days later can be found by interpolating between the −2.35 percent return (with a cumulative weight of 4.94 percent) and −2.30 percent (with a cumulative weight of 5.3246 percent, interpolated from the values on table 2.3). Solving for the 5 percent VaR: 2.35% − (2.35% − 2.30%)*[(0.05 − 0.0494)/(0.0533− 0.0494)] [<--notice how this formula is correct; it's just the text that needs editing to match!]

= 2.34%.

II.3.8.2 Interpretation of Lambda: There are two terms on the right hand side of (II.3.33). The first term is (1 - λ)*r^2. This determines the intensity of reaction of volatility to market events: the smaller is λ the more the volatility reacts to the market information in yesterday’s return. The second term is λ*σ^2. This determines the persistence in volatility: irrespective of what happens in the market, if volatility was high yesterday it will be still be high today. The closer λ is to 1, the more persistent is volatility following a market shock.

Thus a high λ gives little reaction to actual market events but great persistence in volatility; and a low λ gives highly reactive volatilities that quickly die away. An unfortunate restriction of EWMA models is they assume that the reaction and persistence parameters are not independent; the strength of reaction to market events is determined by 1 − λ and the persistence of shocks is determined by λ. But this assumption is, in general, not empirically justified.

The effect of using a different value of λ in EWMA volatility forecasts can be quite substantial. For instance, Figure II.3.6 compares two EWMA volatility estimates/forecasts of the S&P 500 index, with λ = 0.90 and λ = 0.96. We can see from the figure that there are several instances when the two EWMA estimates differ by as much as 5 percentage points.

So which is the best value to use for the smoothing constant? How should we choose λ? This is not an easy question. Statistical methods may be considered: for example, λ could be chosen to minimize the root mean square error between the EWMA estimate of variance and the squared return. But more often λ is often chosen subjectively. This is because the same value of λ has to be used for all elements in a EWMA covariance matrix, otherwise the matrix is not guaranteed to be positive semi-definite. If the value of lambda is chosen subjectively the values usually range between about 0.75 (volatility is highly reactive but has little persistence) and 0.98 (volatility is very persistent but not highly reactive)."