This might be a stupid question, but I just gotta clarify!

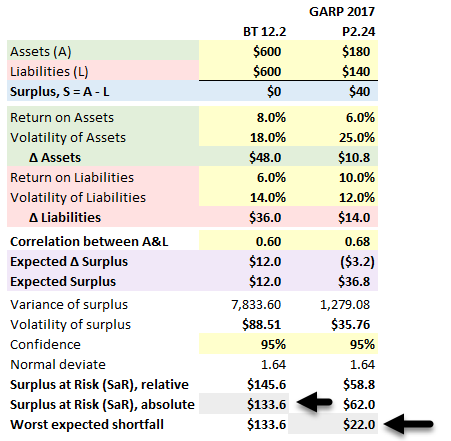

5. An analyst reports the following fund information to the advisor of a pension fund that currently invests in government and corporate bonds and carries a surplus of USD 10 million:

Pension Assets Pension Liabilities

Amount (in USD million) 100 90

Expected Annual Growth 6% 7%

Modified Duration 12 10

Annual Volatility of Growth 10% 5%

To evaluate the sufficiency of the fund's surplus, the advisor estimates the possible surplus values at the end of one year. The advisor assumes that annual returns on assets and the annual growth of the liabilities are jointly normally distributed and their correlation coefficient is 0.8. The advisor can report that, with a confidence level of 95%, the surplus value will be greater than or equal to:

a. USD -11.4 million

b. USD -8.3 million

c. USD -1.7 million

d. USD 0 million

Correct Answer: c

Rationale: The lower bound of the 95% confidence interval is equal to: Expected Surplus - (95% confidence factor * Volatility of Surplus). The required variables can be calculated as follows:

Variance of the surplus = 100^2 * 10%^2 + 90^2 * 5%^2 - 2 * 100 * 90 * 10% * 5% * 0.8 = 48.25

Volatility of the surplus = √48.25 = 6.94,

The expected surplus = 100 * 1.06 - 90 * 1.07 = 9.7.

Therefore, the lower bound of the 95% confidence interval = 9.7 - 1.645 * 6.94 = -1.725

Why is the variance of the surplus calculated as 100^2 * 10%^2 + 90^2 * 5%^2 - 2 * 100 * 90 * 10% * 5% * 0.8

and not 100^2 * 10%^2 + 90^2 * 5%^2 + 2 * 100 * 90 * 10% * 5% * 0.8.

Regards

5. An analyst reports the following fund information to the advisor of a pension fund that currently invests in government and corporate bonds and carries a surplus of USD 10 million:

Pension Assets Pension Liabilities

Amount (in USD million) 100 90

Expected Annual Growth 6% 7%

Modified Duration 12 10

Annual Volatility of Growth 10% 5%

To evaluate the sufficiency of the fund's surplus, the advisor estimates the possible surplus values at the end of one year. The advisor assumes that annual returns on assets and the annual growth of the liabilities are jointly normally distributed and their correlation coefficient is 0.8. The advisor can report that, with a confidence level of 95%, the surplus value will be greater than or equal to:

a. USD -11.4 million

b. USD -8.3 million

c. USD -1.7 million

d. USD 0 million

Correct Answer: c

Rationale: The lower bound of the 95% confidence interval is equal to: Expected Surplus - (95% confidence factor * Volatility of Surplus). The required variables can be calculated as follows:

Variance of the surplus = 100^2 * 10%^2 + 90^2 * 5%^2 - 2 * 100 * 90 * 10% * 5% * 0.8 = 48.25

Volatility of the surplus = √48.25 = 6.94,

The expected surplus = 100 * 1.06 - 90 * 1.07 = 9.7.

Therefore, the lower bound of the 95% confidence interval = 9.7 - 1.645 * 6.94 = -1.725

Why is the variance of the surplus calculated as 100^2 * 10%^2 + 90^2 * 5%^2 - 2 * 100 * 90 * 10% * 5% * 0.8

and not 100^2 * 10%^2 + 90^2 * 5%^2 + 2 * 100 * 90 * 10% * 5% * 0.8.

Regards

")