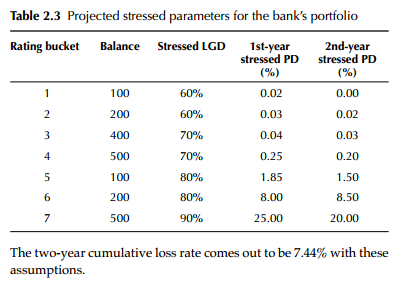

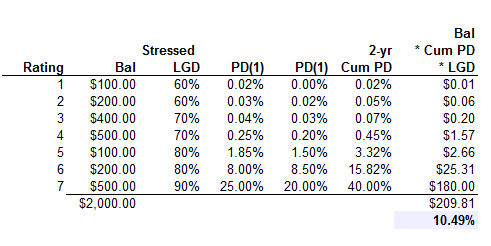

Hi David, in your note (chapter 2) for (Siddique and Hasan stress testing pg 13), the value for two year cumulative rate is 7.44%. However, the GARP official text (pg 303) gave a value of 10.61%. How do we get the value for two year cumulative loss rate and which is the correct value?

Stress testing and other risk management tools

- Thread starter lowhueyyi

- Start date