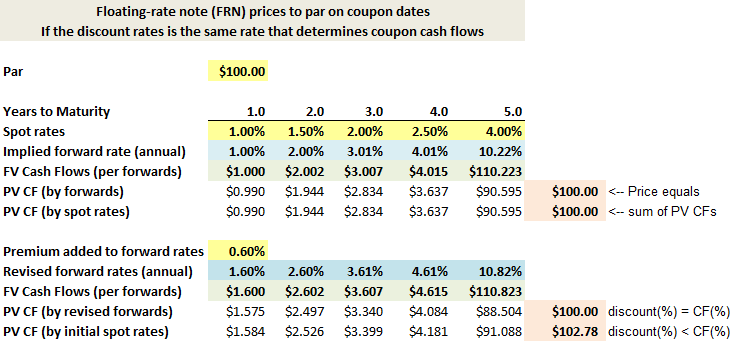

Hi @David Harper CFA FRM

I'm quite confused on why when computing the present value of the floating leg only the notional amount and the LIBOR that corresponds to the last payment date is considered. I don't understand why we don't consider all the other LIBOR rates in the corresponding pay dates.

Can someone please explain why this is the case?

For instance, if we have a 1 million notional swap with a floating rate based on 6-month LIBOR and swap has remaining life of 15 months with pay dates at 3,9,15 months. Spot LIBOR rates are 5.4% at 3 months, 5.6% at 9 months and 5.8% at 15 months. LIBOR at last payment date was 5%.

Then it says that the present value of the floating leg is (1 million + 1 million * .05/2) / 1.054^0.25.

I don't understand the above logic. Why are we not considering the other dates? e.g. why there are no intermediate cash flows for the floating rate?

I'm quite confused on why when computing the present value of the floating leg only the notional amount and the LIBOR that corresponds to the last payment date is considered. I don't understand why we don't consider all the other LIBOR rates in the corresponding pay dates.

Can someone please explain why this is the case?

For instance, if we have a 1 million notional swap with a floating rate based on 6-month LIBOR and swap has remaining life of 15 months with pay dates at 3,9,15 months. Spot LIBOR rates are 5.4% at 3 months, 5.6% at 9 months and 5.8% at 15 months. LIBOR at last payment date was 5%.

Then it says that the present value of the floating leg is (1 million + 1 million * .05/2) / 1.054^0.25.

I don't understand the above logic. Why are we not considering the other dates? e.g. why there are no intermediate cash flows for the floating rate?

Last edited: