Hi everybody,

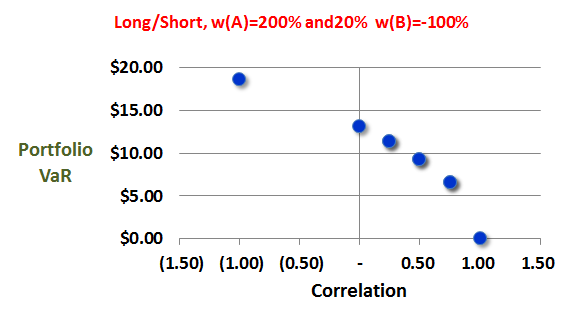

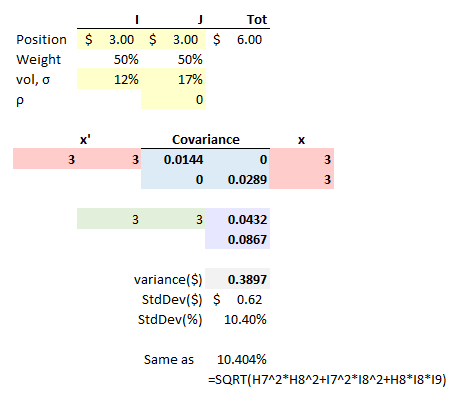

I am confused about a concept in chapter 7 of Jorion. In study notes (topic 52, 2012 edition), there is a sentence "both a correlation of zero and one will place a lower and upper bound on the portfolio total VaR". I can understand one will act as upper bound. How about -1, which I think will be lower bound instead of zero? Thanks!

I am confused about a concept in chapter 7 of Jorion. In study notes (topic 52, 2012 edition), there is a sentence "both a correlation of zero and one will place a lower and upper bound on the portfolio total VaR". I can understand one will act as upper bound. How about -1, which I think will be lower bound instead of zero? Thanks!