@AbchaudhHi @David Harper CFA FRM , @Nicole Seaman,it is my bad the error is in question set of Hull page no.138. Sorry I wrongly tagged it as a error in notes but it is in Question set. If you look at the highlighted text in the below document it says 0.5*30^2*0.0035 = 0.55125% . But it should read "0.5*30^2*0.0035^2 = 0.55125%".

Sorry once again for my mistake to give the reference of the document.

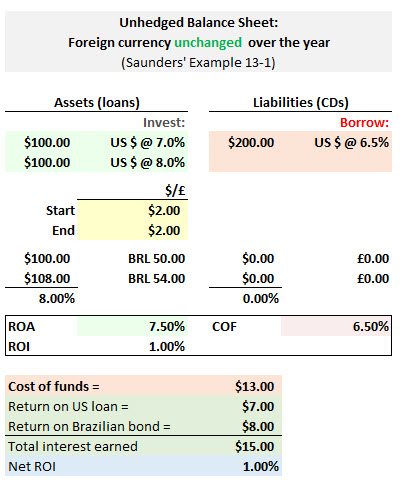

View attachment 1530

Thanks,

Abhishek

Thank you for confirming that it is an error in the PQ set. This error has been pointed out and tagged in the correct PQ forum thread already, so it is on our list to correct in the updated version that we will publish shortly.

Thank you,

Nicole

")

it is a funded purchase: you pay cash to own the share. Derivatives (sans collateral consideration) are unfunded: you promise to make a future payment depending on some formulaic reference to a notional amount; as you don't use your cash, you gain automatic leverage. Hence, the funding of principal versus the reference to (unfunded) notional. The thematic keyword groupings are something like: "cash (spot) funded principal not-leveraged" versus "derivative unfunded notional leveraged." Thanks!

it is a funded purchase: you pay cash to own the share. Derivatives (sans collateral consideration) are unfunded: you promise to make a future payment depending on some formulaic reference to a notional amount; as you don't use your cash, you gain automatic leverage. Hence, the funding of principal versus the reference to (unfunded) notional. The thematic keyword groupings are something like: "cash (spot) funded principal not-leveraged" versus "derivative unfunded notional leveraged." Thanks!

")