Eustice_Langham

Active Member

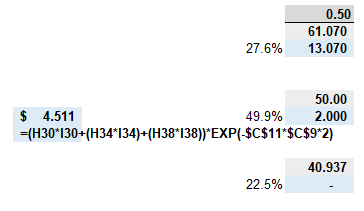

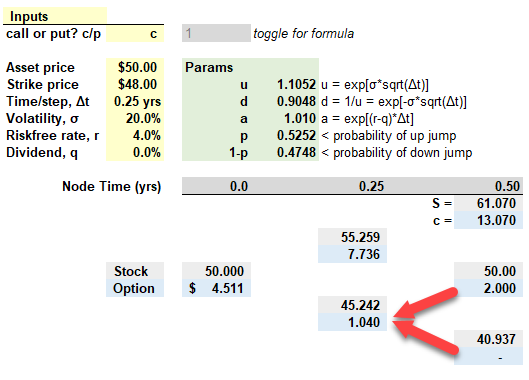

Hi, I hope that someone can assist with the below question that is in the GARP Notes:

14.11 A stock price is currently 40. It is known that it will be 42 or 38 at the end of a month. The risk-free rate is 4% per annum with continuous compounding. What is the value of a one-month call option with a strike price of 39?

14.12 In Question 14.11, what position should be taken in the stock to hedge a short position in the option?

I have been able to arrive at the answer for question 14.11, ie 1.595

However the answer for 14.12 is something that I am struggling with, the answer according to the notes is as follows:

"The position is long 0.75 of a share. This is because a portfolio of 0.75 shares and short one option is worth 28.5 for both outcomes"

Could someone explain how this was arrived at? Thanks

14.11 A stock price is currently 40. It is known that it will be 42 or 38 at the end of a month. The risk-free rate is 4% per annum with continuous compounding. What is the value of a one-month call option with a strike price of 39?

14.12 In Question 14.11, what position should be taken in the stock to hedge a short position in the option?

I have been able to arrive at the answer for question 14.11, ie 1.595

However the answer for 14.12 is something that I am struggling with, the answer according to the notes is as follows:

"The position is long 0.75 of a share. This is because a portfolio of 0.75 shares and short one option is worth 28.5 for both outcomes"

Could someone explain how this was arrived at? Thanks

")