In the forum this week (selected subset only)

- Risk typology (P1.T1): Is this true or false: To obtain firm-wide risk, we should aggregate market, credit and operational risks but exclude business risks https://forum.bionicturtle.com/threads/p1-t1-601-risk-governance-at-a-bank.9215/

- Bond pricing (P1.T3): Arbitrage and the Law of One Price in bond pricing https://forum.bionicturtle.com/threads/fmp.9114/

- Cost of carry (P1.T3): On the direct link between storage cost as constant ratio of asset price (u) and lumpy storage costs (U) https://forum.bionicturtle.com/threads/storage-costs-hull-vs-mcdonalds.9931/

- Reducing portfolio beta with futures contracts (P1.T3): GARP 2009 P2.Q1. The current value of the S&P 500 index is 1457, and each S&P futures contract is for delivery of USD 250 times the index. A long‐only equity portfolio with market value of USD 300,100,000 has beta of 1.1. To reduce the portfolio beta to 0.75, how many S&P futures contract should you sell? http://www.analystforum.com/forums/frm-forum/91354536

- Forex (P1.T3): Is AVERAGE assets the denominator of net interest margin (NIM) in Saunders’ FX hedge? https://forum.bionicturtle.com/threads/p1-t3-502-foreign-exchange-fx-hedges.8809/page-2#post-45740

- Commodities (P1.T3): Crude oil crack spread questions that I can’t answer https://forum.bionicturtle.com/threads/l1-t3-189-commodity-spreads-and-basis-risk.4671/

- Exotic options (binary, P1.T3): On the difference between N(d1) and N(d2): Why is the price of a cash-or-nothing binary given by Q*e^(-rT)*N(d2) but the asset-or-nothing binary price is given by S*N(d1)? https://forum.bionicturtle.com/threads/probability-of-being-itm.9932/ Brilliant help from @ShaktiRathore!

- Value at risk: What is full repricing (P1.T4) http://www.analystforum.com/forums/frm-forum/91354514

- VaR mapping fixed income (P2.T5): Duration mapping can tricky, what are the vertices? What are the risk factors? https://forum.bionicturtle.com/threads/p2-t5-208-var-mapping-topic-review.6069/

- Term structure models (P2.T5): @Rusenuhu’s very cool demonstration of why should we scale the interest rate tree with r[12,12] = r(0)+12*sigma*SQRT(1/12) rather than perhaps the more expected r[12,12]=r(0)+sigma*SQRT(12/12) https://forum.bionicturtle.com/thre...odels-with-and-without-drift.6683/#post-45644

- Credit (P2.T6) : On similarity between Hull’s and Malt’z single factor credit value at risk (CVaR) model https://forum.bionicturtle.com/thre...ng-single-factor-model-malz-section-8-4.6979/

- Counterparty credit (P2.T6): Great observation by The Great Kahn (love his handle!) about 98% versus 95% potential future exposure (PFE) https://forum.bionicturtle.com/threads/p2-t6-413-credit-exposure-profiles.7774/#post-45759

- Credit value at risk (P2.T6): Does or does not CVaR include expected losses? https://forum.bionicturtle.com/threads/var-and-expected-loss.9933/

- Credit value adjustment (P2.T6) Is the credit value adjustment (CVA) in counterparty risk an addition or subtraction, and how do we know to whose counterparty perspective is being referenced? https://forum.bionicturtle.com/threads/p2-t6-206-counterparty-risk-cva-topic-review.6184/#post-45722

- Surplus at risk (P2.T8): In surplus at risk (SaR), why exactly does Jorion use volatility of the surplus” as an input? (Spoiler alert: so there is only one volatility rather than one each for assets and liabilities) https://forum.bionicturtle.com/threads/p2-t8-12-surplus-at-risk-sar.5488/page-2#post-45634

- Investment (P2.T8): How is the test of alpha derived? https://forum.bionicturtle.com/thre...on-frm-handbook-topic-review.7723/#post-45747

- Regression (P2.T8): Bodie’s elegant approach to retrieving correlation (or R^2) from the single-factor model https://forum.bionicturtle.com/thre...-significance-of-alpha.5578/page-2#post-45639

- RAROC (P2.T8): Risk-adjusted return on capital does not have a single magic definition, really; there are several flavors of return on capital. The criteria is ratio consistency https://forum.bionicturtle.com/threads/p2-t7-300-economic-capital-topic-review.6830/

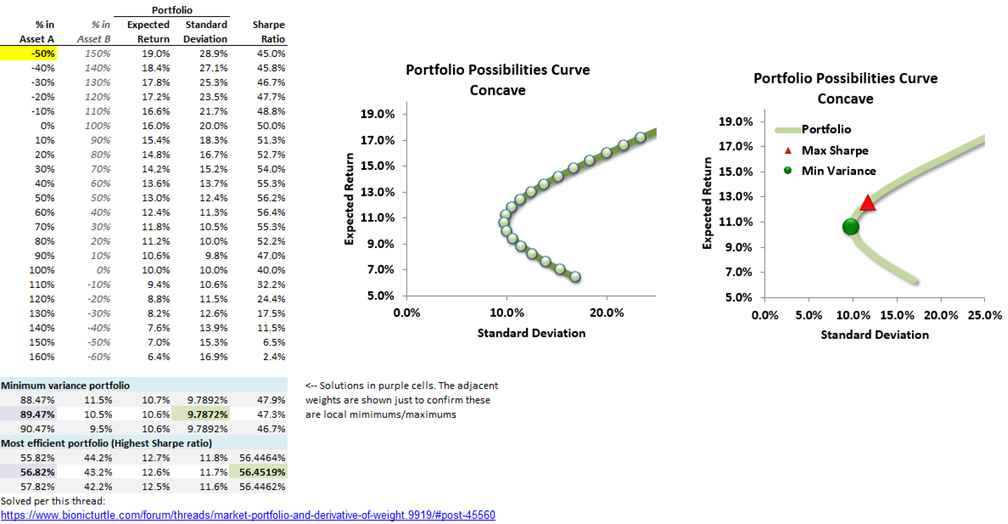

- Portfolio VaR (P2.T8): Portfolio VaR measures tend to utilize covariance properties, including the self-referencing covariance between a position and its own portfolio https://forum.bionicturtle.com/thre...nent-value-at-risk-var.4779/page-2#post-45627

- EU Eyes Tailoring Global Capital Rules to Spare Ailing Banks http://www.bloomberg.com/news/artic...lobal-capital-rules-to-spare-struggling-banks

- Financial Crimes Enforcement Network (FinCEN): Advisory to Financial Institutions on Cyber-Events and Cyber-Enabled Crime http://trtl.bz/2efHiTo

- The Federal Reserve Board announced on Monday it has voted to affirm the Countercyclical Capital Buffer (CCyB) at the current level of 0 percent http://www.federalreserve.gov/newsevents/press/bcreg/20161024a.htm

- Bundesbank Says High-Frequency Trading Can Enhance Volatility http://www.bloomberg.com/news/artic...high-frequency-trading-can-enhance-volatility “The Bundesbank divided high-frequency firms into two broad types: those that trade actively on news, and those that act as market-makers, or intermediaries between buyers and sellers of assets. It found that the first type of traders were particularly active during periods of high market volatility, and therefore contributed to that volatility. The second group, by contrast, tended to withdraw from financial markets during periods of high market stress—just when they might be needed most to provide additional liquidity.”

- BNP’s Capital Relief Should Be Contagious (Rule change gives more breathing room before coupons and dividends are threatened) http://www.wsj.com/articles/bnps-capital-relief-should-be-contagious-1477666901 “The reason for the change: European regulators have altered how they structure capital requirements known as the Supervisory Review and Evaluation Procedure, or SREP, to make them more like U.K. requirements. This involves splitting one element of the requirement—a supervisory add-on known as pillar 2—into one public part that banks must always meet, and one nonpublic part that regulators use as an extra guard against things they don’t like about an individual bank or how it is run. Privately, regulators still have a higher number for BNP than its 8% SREP level.”

- Explaining the October Flash Crash in the British Pound http://www.visualcapitalist.com/october-flash-crash-british-pound/

- Blockchain Hype Takes Hit as Chain Releases Code for All to Use http://www.garp.org/#!/risk-intelligence/detail/a1Z40000003LmomEAC Refers to this, Announcing Chain Core Developer Edition https://blog.chain.com/announcing-chain-core-developer-edition-77255e3c1a64#.kfa47midu

- Lemonade: Insurance Is Changed Forever http://insurancethoughtleadership.com/lemonade-insurance-will-never-be-the-same/ “The thing to know about Lemonade is that it has built a full-stack insurance model from the ground up. This is NOT a mobile app sitting on top of traditional insurance.”

- What’s Your Business’s Cyber Risk Score? http://www.fico.com/en/blogs/fraud-...in-the-nascent-cyber-breach-insurance-market/ “Analytic software firm FICO today launched the FICO® Enterprise Security Score, a metric that reveals the likelihood an organization will be breached due to a cyber attack. This score can be used by an enterprise to understand and shore up its defense gaps, and by third parties such as cyber insurance providers, potential partners and customers who need an objective measure of a firm’s cyber risk.”

- Cyber Defense in an Imperfect World, a New Approach http://www.brinknews.com/cyber-defense-in-an-imperfect-world-a-new-approach/ “Most current strategies of cyber defense usually incorporate a five-stage cycle of risk management components: 1. Identify the most critical assets, 2. Protect by controlling access, 3. Detect any intrusions, 4. Respond to contain the intrusion, and 5. Recover by restoring to normal operation.

- This framework is solid, but poses challenges; thinking outside the box might make for a good number six on the risk management matrix.”

- Borrower or Fraudster? Online Lenders Scramble to Tell the Difference http://www.wsj.com/articles/borrowe...rs-scramble-to-tell-the-difference-1477580637 and, related: New Consortium of Online Lending Leaders Aims to Combat Fraud (Online Lending Network aims to curb fraud, making loan stacking a thing of the past) http://www.lendacademy.com/online-lending-network-combat-fraud/

- Exxon Warns on Reserves as It Posts Lower Profit (Oil producer to examine whether assets in an area devastated by low prices and environmental concerns should be written down) http://www.wsj.com/articles/exxon-mobil-profit-revenue-slide-again-1477657202 and Exxon Concedes It May Need to Declare Lower Value for Oil in Ground http://www.nytimes.com/2016/10/29/b...to-declare-lower-value-for-oil-in-ground.html “On Friday, though, the company acknowledged that it faced what could be the biggest accounting revision of reserves in its history. Exxon Mobil might have to concede that 3.6 billion barrels of oil-sand reserves and one billion barrels of other North American reserves are currently not profitable to produce.”

- Welcome to the first edition of our Climate Bonds Standard & Certification Newsletter http://www.climatebonds.net/2016/10/new-climate-bonds-standard-certification-newsletter

- CRO Interview: A View from Zurich (Chief risk officer since mid-2015, Cecilia Reyes points to a clearer mandate for risk management and improved peer relations with risk owners – the businesses) http://www.garp.org/#!/risk-intelligence/detail/a1Z40000003LyoREAS/cro-interview-view-from-zurich

- Managing Trading Desk Risk: Physiology Beats Out Bias Tracking (Researcher John Coates finds that understanding “gut feelings” adds dimensions that go beyond the past contributions of behavioral finance) http://www.garp.org/#!/risk-intelli...-desk-risk-physiology-beats-out-bias-tracking

- Risk Culture: What Matters Most? (The standard bifurcation of business and risk responsibilities arguably hurts, rather than helps, the goal of creating a strong risk culture. How do we fix that?) http://www.garp.org/#!/risk-intelligence/detail/a1Z40000003Lz66EAC/risk-culture-what-matters-most

- Wall Street’s Frantic Push to Hire Coders http://www.bloomberg.com/news/artic...rs-wanted-elite-college-degrees-not-necessary “This is Wall Street’s new tech meritocracy. Financial institutions traditionally coveted graduates from Stanford and other big-name schools and people already working in Silicon Valley. But that system tends to overlook good programmers from other schools or gifted dropouts, according to recruiters. And besides, banks need to fill so many programming jobs that elite schools can’t possibly pump out enough candidates.”

- Janet Tavakoli: Life And Death On Wall Street https://www.peakprosperity.com/podcast/102990/janet-tavakoli-life-and-death-wall-street Her book (Decisions: Life and Death on Wall Street) is here http://amzn.to/2f1kl7R

- Extreme Events in Finance: A Handbook of Extreme Value Theory and its Applications (Wiley Handbooks in Financial Engineering and Econometrics) 1st Edition https://www.amazon.com/dp/1118650190/?tag=bt077d-20

- Quantitative Stock Analysis Tutorial: Screening the returns for every S&P 500 Stock in less than 5 minutes http://www.mattdancho.com/investments/2016/10/23/SP500_Analysis.html

- corrr 0.2.1 now on CRAN https://drsimonj.svbtle.com/corrr-021-now-on-cran

- Better Confidence Intervals for Quantiles http://staff.math.su.se/hoehle/blog/2016/10/23/quantileCI.html

- Citigroup Trading Desk Made $300 Million on Rate Swaps http://www.bloomberg.com/news/artic...g-desk-said-to-reap-300-million-on-rate-swaps Just as John Hull describes in Using the Swap to Transform a Liability: “Weber’s team also has been minting revenue tied to the bank’s handling of corporate bond deals by working with clients issuing the debt, according to the people. In such cases, companies typically sell debt to investors with a fixed interest rate, then enter a contract with the bank to pay a variable rate.”

- Citigroup’s $300 Million Windfall Spotlights Swap Dispute https://www.bloomberg.com/gadfly/ar...-300-million-windfall-spotlights-swap-dispute

- Volatility Has Currency Traders Abandoning Stop-Loss Orders (In sharp swings, automated orders meant to protect against losses are often making them worse) http://www.wsj.com/articles/market-...s-abandoning-a-tool-to-stop-losses-1477560601

- Swap Traders and Stop Orders https://www.bloomberg.com/view/articles/2016-10-28/swap-traders-and-stop-orders “How can a bank make $300 million in trading if it's not "prop"? And the answer is always sort of obvious, though not universally satisfying. Clients want to do interest-rate swaps. There's a lot of demand. Swaps aren't quite like stocks; you don't buy 100 swaps from a customer one second and sell them to another customer the next. They are principal trades, often with terms of many years; you enter into a swap and then you just ... have it.”

- Masters in Business (MiB): Aswath Damodaran of NYU Stern http://ritholtz.com/2016/10/171004/

- The failure of covered interest parity: FX hedging demand and costly balance sheets (BIS Working Papers) http://www.bis.org/publ/work590.htm

- Ratings Inflation Is Back, Subprime Style http://www.bloomberg.com/news/artic...t-pedal-risks-in-biggest-ever-borrowing-binge

- Austria 70-Year Bond Hands Out Duration Lesson in First Week http://www.bloomberg.com/news/artic...-bond-dishes-out-duration-lesson-on-first-day “Its relatively low coupon and long maturity help produce a high duration factor, meaning it’s price is more volatile … The duration on Bank of America’s Global Government Bond Index climbed to an all-time high of about 8.5 in July, from about 5 when the benchmark began in 1997. Austria’s 70-year bonds have a duration of 43, according to data compiled by Bloomberg.”

- Basel III – Capital Adequacy – US Implementation – Credit Risk Weights for Internal Ratings Based and Advanced Measurement Approaches http://trtl.bz/2f5x3QE

- How to ‘Gamify’ Risk Management http://insurancethoughtleadership.com/how-to-gamify-risk-management/

- Is Longevity Insurance Too Risky? http://www.wsj.com/articles/is-longevity-insurance-too-risky-1477274761

- Eighth edition of Risk Perspectives (This edition continues the theme started in the previous one – convergence of risk, finance, and accounting disciplines) http://www.moodysanalytics.com/Publ...2016/Convergence-Risk-Finance-Accounting-CECL Issue is here http://trtl.bz/2f5bAr8

- Chief Investment Officer’s 2016 Risk Parity Investment Survey http://www.ai-cio.com/2016-Risk-Parity-Investment-Survey/

- Why Math Education in the U.S. Doesn't Add Up (Research shows that an emphasis on memorization, rote procedures and speed impairs learning and achievement) https://www.scientificamerican.com/article/why-math-education-in-the-u-s-doesn-t-add-up/

Last edited by a moderator: