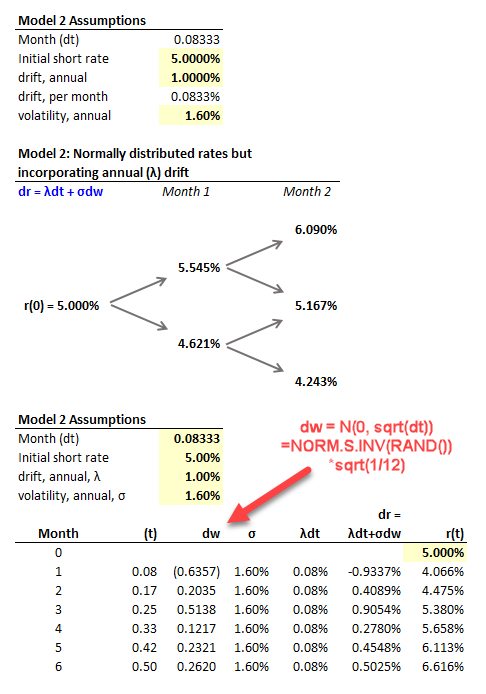

Hi David. A question from reading reading 40 on P2.T5, page 42. The table regarding Model 2; Simulation, the annual drift is converted into a monthly drift by dividing by 12. However, the annual volatility is not converted into monthly volatility. Page 43 is saying that the annual volatility should be multiplied by SQRT (1/12) to get the monthly volatility. Is this because the dw is already time-scaled?

Tuckman: Model 2: Simulation

- Thread starter CarlosB

- Start date