Unusualskill

Member

Hi,

Below is the question that I came across while reading Part 1 FRM Swap:

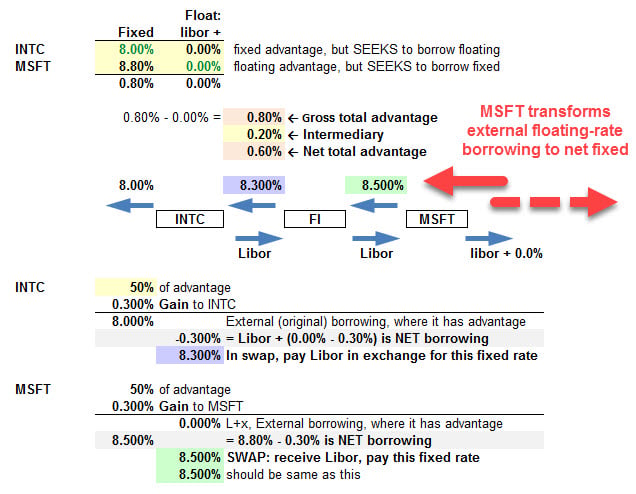

Which of the following would properly transform a floating-rate liability to a fixed-rate liability? Enter into a pay:

A. Foreign currency swap

B. Fixed interest rate swap

C. Domestic currency swap

D. Floating interest rate swap

May I ask what are the differences of the above swaps as I know when enter into currency swap, there are both fixed and floating but I never come across foreign currency , domestic currency.

Also, Fixed interest rate swap and floating interest rate swap here means pay fixed interest and pay floating interest respectively?

Thank you!

Below is the question that I came across while reading Part 1 FRM Swap:

Which of the following would properly transform a floating-rate liability to a fixed-rate liability? Enter into a pay:

A. Foreign currency swap

B. Fixed interest rate swap

C. Domestic currency swap

D. Floating interest rate swap

May I ask what are the differences of the above swaps as I know when enter into currency swap, there are both fixed and floating but I never come across foreign currency , domestic currency.

Also, Fixed interest rate swap and floating interest rate swap here means pay fixed interest and pay floating interest respectively?

Thank you!

), thanks,

), thanks,