Learning outcomes: Describe the key features of the various categories of insurance companies and identify the risks facing insurance companies. Describe the use of mortality tables and calculate the premium payment for a policy holder. Distinguish between mortality risk and longevity risk and describe how to hedge these risks.

Questions:

21.3.1. Most insurance is written by either life/annuity, health, or property/casualty (aka, non-life) insurance companies. Insurance transfers risk from an individual or company to the insurance company. Which of the following statements is TRUE?

a. Variable life insurance exposes the policyholder to investment risk

b. Whole life insurance exposes the insurance company to longevity risk

c. Term life insurance exposes the insurance company to inflation risk

d. Property-casualty insurance exposes the insurance company to mortality risk

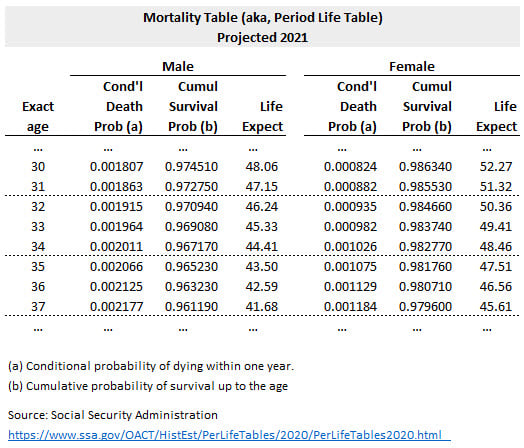

21.3.2. The mortality table (aka, period life table) below was extracted from actual 2021 projections by the U.S. Social Security Administration. For males and females age 30 to 37, inclusive, this table shows the conditional probability of death within one year, the cumulative survival probability, and the life expectancy.

Let's assume that an insurance company uses this table to price a two-year term life insurance policy with a face value of USD $1.0 million for a female policyholder who is 34 years old. The discount rate is 6.0% per annum with annual compounding. Which is nearest to the minimum annual premium that should be charged by the company (note: inspired by GARP's EOC PQ 2.12)?

a. $97.50

b. $330.40

c. $1,020.00

d. $5,040.00

21.3.3. Acme Industrial Corporate is the plan sponsor for a defined benefit pension plan. At the time of their retirements, participants are promised an annual benefit that is the product of three components: 1.5% * Number of years of service * Average three-year salary. To hedge its exposure to longevity risk, Acme seeks to employ derivatives. Let "MR" represent a mortality rate. Which of the following is the best hedge against Acme's longevity risk with respect to the defined benefit pension plan?

a. A longevity swap where Acme periodically Pays a Fixed premium and Receives Notional Principal × (Realized MR - Prespecified MR)

b. A longevity swap where Acme periodically Pays a Fixed premium and Receives Notional Principal × (Prespecified MR - Realized MR)

c. A longevity option that Acme purchases (long option) and that has a payoff equal to max(0, Realized MR - Prespecified MR)

d. A longevity option that Acme sells/write (short option) and that has a payoff equal to max(0, Prespecified MR - Realized MR)

Answers here:

Questions:

21.3.1. Most insurance is written by either life/annuity, health, or property/casualty (aka, non-life) insurance companies. Insurance transfers risk from an individual or company to the insurance company. Which of the following statements is TRUE?

a. Variable life insurance exposes the policyholder to investment risk

b. Whole life insurance exposes the insurance company to longevity risk

c. Term life insurance exposes the insurance company to inflation risk

d. Property-casualty insurance exposes the insurance company to mortality risk

21.3.2. The mortality table (aka, period life table) below was extracted from actual 2021 projections by the U.S. Social Security Administration. For males and females age 30 to 37, inclusive, this table shows the conditional probability of death within one year, the cumulative survival probability, and the life expectancy.

Let's assume that an insurance company uses this table to price a two-year term life insurance policy with a face value of USD $1.0 million for a female policyholder who is 34 years old. The discount rate is 6.0% per annum with annual compounding. Which is nearest to the minimum annual premium that should be charged by the company (note: inspired by GARP's EOC PQ 2.12)?

a. $97.50

b. $330.40

c. $1,020.00

d. $5,040.00

21.3.3. Acme Industrial Corporate is the plan sponsor for a defined benefit pension plan. At the time of their retirements, participants are promised an annual benefit that is the product of three components: 1.5% * Number of years of service * Average three-year salary. To hedge its exposure to longevity risk, Acme seeks to employ derivatives. Let "MR" represent a mortality rate. Which of the following is the best hedge against Acme's longevity risk with respect to the defined benefit pension plan?

a. A longevity swap where Acme periodically Pays a Fixed premium and Receives Notional Principal × (Realized MR - Prespecified MR)

b. A longevity swap where Acme periodically Pays a Fixed premium and Receives Notional Principal × (Prespecified MR - Realized MR)

c. A longevity option that Acme purchases (long option) and that has a payoff equal to max(0, Realized MR - Prespecified MR)

d. A longevity option that Acme sells/write (short option) and that has a payoff equal to max(0, Prespecified MR - Realized MR)

Answers here: