In the example of Mapping a two-bond portfolio, the spreadsheet used (1-(1+YTM)^-Maturity)*1/YTM, I might've seen this formula in p1 but cannot remember, is this an alternative of calculating mod duration?

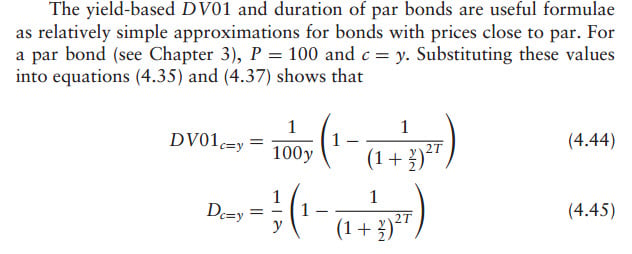

Hi @ziminli1228 Right, it is a convenient formula for modified duration but only for the special case of a bond that is priced at par. See below, Tuckman's 4.45; the "c=y" subscript indicates coupon rate equal to yield and, therefore, a bond that is priced at par. Tuckman's formula, as with his entire text, presumes semi-annual compound frequency. My XLS mimcs Jorion, who is always assuming annual compound frequency, so my version is the annual-equivalent version of 4.45 below, where the only difference is that 1/[(1+y/2)^(2T)] is replaced with 1/(1+y)^T) = (1+y)^-T, just as it would be in pricing. Thanks!

This site uses cookies to help personalise content, tailor your experience and to keep you logged in if you register.

By continuing to use this site, you are consenting to our use of cookies.