Can’t recall the letter sorryOption A?

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Exam Feedback May 2021 Part 2 Exam Feedback

- Thread starter Nicole Seaman

- Start date

-

- Tags

- exam-feedback

- Status

- Not open for further replies.

14. Picked D as well, but wasn’t certainAny feedback on below?

12 : BCVA question ...ans D ? -5K something ? - - > i subtracted the DVA from CVA as i recall, answer was 1,000 something - not sure if right.

14 : some predatory trading , model risk , moral hazard question , was A or D the answer ? guess i selected A --> the frictions question? Not sure if it was adverse selection

15 UL component , correlation was given and total portfolio split as 16K and 24K , guess i selected 131 as answer

15. Adverse selection for sure

16. Cannot recall but if you remember the formula then should have no problem

You’re correctI think the question was stress loss, not stress EL, which is stress EL - EL..I at least hit one answer possibility doing this

Brain just stuck have no idea how to calculate wcl of that question in the exam

ah

Also there’s one question which they have given the buy cost and sale cost and the risk factor something like that, and asked should the investor/ bank sell the equity/bond or increase the holding of it

Anyone know the answer? I have no idea how to do this as well

friction between arranger and originator is a predatory borrowing and lending problem. (it on the pre study Garp question)14: I think it was friction between originator and assigner. I chose adverse as originator has more knowledge on the mortgager than the assigner

FRMNinjaLeonardo

New Member

Choice C: default correlation of the originator (Bank xxx) of the mortgage and the CDO protection (CDS) seller increase.Intial picked up B, Correlation swap as answer.

Then after reading C , Value of cds goes down with increase of correlation. Went with C , with some doubt in mind. Just thinking they didnt mention the direction of correlation swap

I think the originator has nothing to do with the CDO here, as it already transferred the credit risk to the SPV. It would be the default correlation between the underwriter of the CDO and the protection seller that matters. So I chose B as my answer.

ThomasHuang

New Member

Anyone recall the problem about a portfolio of assets starting at 120 with a decreasing number of assets surviving?

Also there was a question about a firm's asset value being close to the level of senior debt (firm also had equity and mezzanine debt).

Also there was a question about a firm's asset value being close to the level of senior debt (firm also had equity and mezzanine debt).

Got D, 15.xx% for the first oneAnyone recall the problem about a portfolio of assets starting at 120 with a decreasing number of assets surviving?

Also there was a question about a firm's asset value being close to the level of senior debt (firm also had equity and mezzanine debt).

ThomasHuang

New Member

Yeah that sounds familiarGot D, 15.xx% for the first one

ThomasHuang

New Member

For the second question there was some mention of the firm having an equal chance of failure or being acquiredAnyone recall the problem about a portfolio of assets starting at 120 with a decreasing number of assets surviving?

Also there was a question about a firm's asset value being close to the level of senior debt (firm also had equity and mezzanine debt).

FRMNinjaLeonardo

New Member

first one, I remember the question was asking "time-weighted discrete default rate", which I calculated using geometric average and get the answer D.Anyone recall the problem about a portfolio of assets starting at 120 with a decreasing number of assets surviving?

Also there was a question about a firm's asset value being close to the level of senior debt (firm also had equity and mezzanine debt).

The second one, is the question saying someone observed the market volatility is increasing, and asking the direction (increase/decrease) of senior debt, mezzanine debt and equity's value?

ThomasHuang

New Member

Yes I also got D for the first question.first one, I remember the question was asking "time-weighted discrete default rate", which I calculated using geometric average and get the answer D.

The second one, is the question saying someone observed the market volatility is increasing, and asking the direction (increase/decrease) of senior debt, mezzanine debt and equity's value?

And that does sound like the premise of the question for the second question.

ThomasHuang

New Member

I actually think it was asset volatility. But I assumed because there was a potential acquisition it would give the equity upsideYes I also got D for the first question.

And that does sound like the premise of the question for the second question.

I remember when the firm is not doing very wellI actually think it was asset volatility. But I assumed because there was a potential acquisition it would give the equity upside

Mezzanine would have the same property as equity

Which both will go up in value in financial distress, while senior debt will fall in value

Ullaskarkera

Member

oops..silly mistake then ;(Choice C: default correlation of the originator (Bank xxx) of the mortgage and the CDO protection (CDS) seller increase.

I think the originator has nothing to do with the CDO here, as it already transferred the credit risk to the SPV. It would be the default correlation between the underwriter of the CDO and the protection seller that matters. So I chose B as my answer.

Ullaskarkera

Member

I also went with equity and subordinate increases...C or DI remember when the firm is not doing very well

Mezzanine would have the same property as equity

Which both will go up in value in financial distress, while senior debt will fall in value

You are correct, I got that wrong lolfriction between arranger and originator is a predatory borrowing and lending problem. (it on the pre study Garp question)

Yeah time weight average default rate, got like 15,39%.first one, I remember the question was asking "time-weighted discrete default rate", which I calculated using geometric average and get the answer D.

The second one, is the question saying someone observed the market volatility is increasing, and asking the direction (increase/decrease) of senior debt, mezzanine debt and equity's value?

same here, mezzanine behaved like equityI remember when the firm is not doing very well

Mezzanine would have the same property as equity

Which both will go up in value in financial distress, while senior debt will fall in value

mariomansour

New Member

Originator and arranger. The arranger (issuer) purchases the loans from the originators for the purpose of resale through securitized products. The arranger will perform due diligence but still operates at an information disadvantage to the originator. That is, the originator has superior knowledge about the borrower (adverse selection problem). In addition, the originator may falsify or stretch the bounds of the application resulting in larger than optimal lending (predatory lending or predatory borrowing).You are correct, I got that wrong lol

So both? Lol

I got your thinking and that’s how I proceed, but GARP practice exercisesOriginator and arranger. The arranger (issuer) purchases the loans from the originators for the purpose of resale through securitized products. The arranger will perform due diligence but still operates at an information disadvantage to the originator. That is, the originator has superior knowledge about the borrower (adverse selection problem). In addition, the originator may falsify or stretch the bounds of the application resulting in larger than optimal lending (predatory lending or predatory borrowing).

So both? Lol

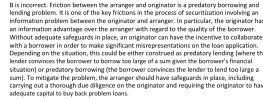

says is predatory lending/borrowing. See bellow:

Attachments

On the other side, the only answer that said “the arranger should perform due diligence on the originator” was the adverse selection choice I believe; anyone recall?Originator and arranger. The arranger (issuer) purchases the loans from the originators for the purpose of resale through securitized products. The arranger will perform due diligence but still operates at an information disadvantage to the originator. That is, the originator has superior knowledge about the borrower (adverse selection problem). In addition, the originator may falsify or stretch the bounds of the application resulting in larger than optimal lending (predatory lending or predatory borrowing).

So both? Lol

- Status

- Not open for further replies.

Similar threads

- Replies

- 4

- Views

- 1K

- Replies

- 0

- Views

- 1K

- Replies

- 4

- Views

- 3K

- Replies

- 1

- Views

- 1K

- Replies

- 1

- Views

- 1K