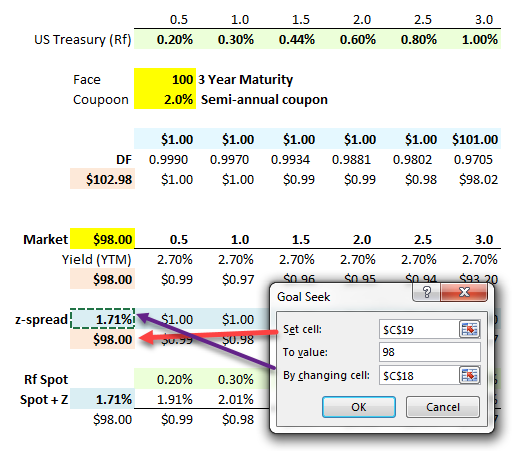

Hi @David Harper CFA FRM, I am a little confused with the first tab on excel. How did you calculate the z spread to get 1.71%? It's not linked with formula so I'm guessing you prob use solver?

Hi @Linghan The XLS could be clearer, sorry. See screenshot below. I only needed Goak Seek: solving for bond price ("Set cell") equal to 98.8 by changing the z-spread. You can see that Row 19 discounts the bond's cash flows by multiplying by 1/(1+(S+Z)/2)^(T*2); in this way, the z-spread is the value that, when added to the risk-free spot rate (given by S), will produced a discounted value equal to the "observed" price of $98.00. To my knowledge, this requires an iterative (goal seek, solver) type solution .... I hope that clarifies, thanks for looking at it!

Hi @David Harper CFA FRM , wanted to clarify (this is a dumb question). Are we expected to calculate the z-spread w/ our calculator on the Part II exam?

Hi @trigg989 I was thinking about this because Tuesday we publish a quiz (part of a new interactive credit quiz series) and i allocated a question to z-spread (because it is a Malz concept and it is an important spread concept) . So my upcoming 710.3 does ask for a z-spread approximation by using duration (that is, duration is a single factor approximation such that it can be used to approximate the z-spread, I realized and my simulations did confirmed; but it makes intuitive sense because duration assumes a parallel shift in the yield curve). I mention that because, to your question, I could not find or generate a "fair" z-spread question that could be somewhat easily answered without excel (given that it requires an iteration to solve). However, there is one obvious exception and, therefore, one obvious exam-worthy candidate: if the assumption is given that the risk-free zero (aka, spot) rate curve is flat, then it's easy to imagine a fair question. For example,

[and this is the one I almost wrote Tuesday, and will eventually include in the new credit set] If the zero (aka, spot) rate curve is flat at 2.0% per annum with semi-annual compounding, what is the z-spread on a five-year $100.00 fair value bond that pays a semi-annual coupon of 3.0% when its price is $97.00. Answer: this bond's yield is given by N = 10, PV = -97, PMT = 1.5, FV = 100 and CPT I/Y = 1.831 * 2= 3.66%; and only in this special case where the risk-free curve is flat can we simply deduct 2.0% to retrieve the z-spread of 1.66%. This is the only realistic example that i can think of. So, i think the answer to your question is: no, you would not be expected to find a z-spread except where the risk-free curve is flat (because if the Rf curve is flat, then the z-spread equals "nominal yield spread" or what Malz simply calls the "yield spread"). I hope that helps!

This site uses cookies to help personalise content, tailor your experience and to keep you logged in if you register.

By continuing to use this site, you are consenting to our use of cookies.