P1 or P2.

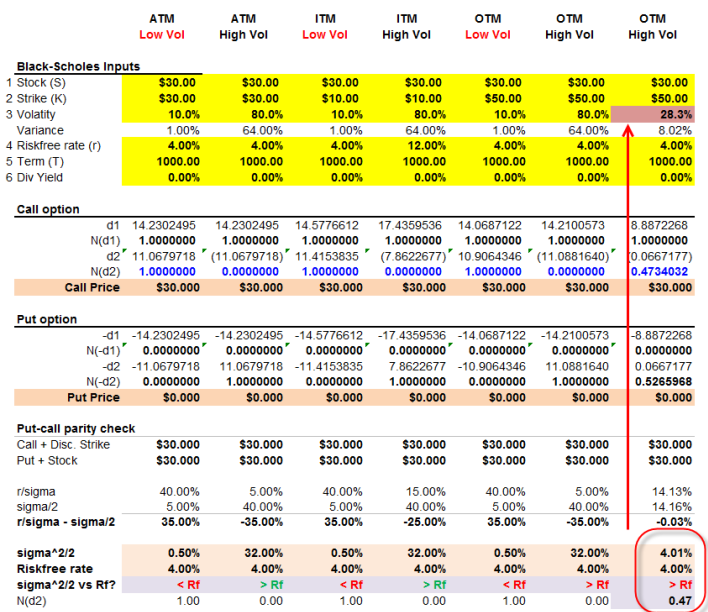

@[email protected] posted another provocative question here. She observes:

Questions:

@[email protected] posted another provocative question here. She observes:

According to Hull as the time to expiration increases, options become more valuable. [But] when I check this with the Black Scholes formula: Put = K*exp(-rT)*N(-d2)-S*N(-d1), it appears that N(-d2) tends to 1; N(-d1) tends to zero, and exp(-rT) tends to zero ... I conclude that the put price tends to zero.

Questions:

- Is she mathematically correct and, if so, what is a (relatively) simple interpretation?

- Does a call option have a similar limit/asymptote (as term extends) at zero? If so/not, what is a similar interpretation?