gargi.adhikari

Active Member

Hi,

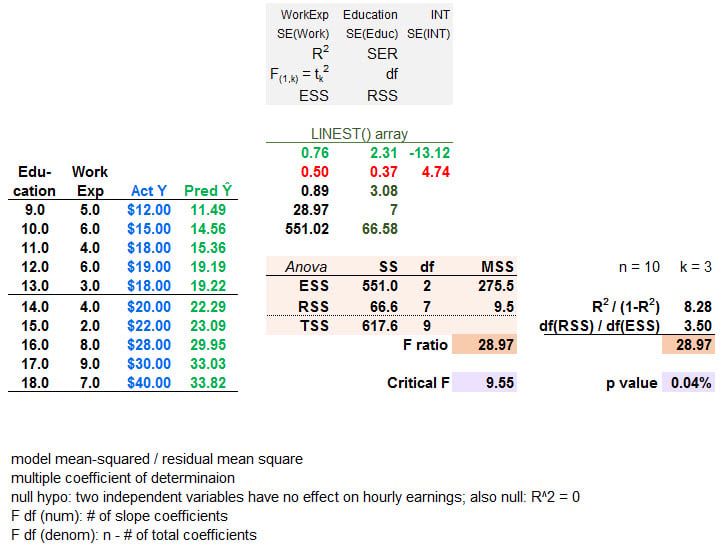

@David Harper CFA FRM had indicated in a thread that -" The general form of the F-statistic is F[numerator df, denominator df] = (ESS/df)/(RSS/df) "

F -Statistic is also expressed as = {Sum Of Squares BETWEEN / df-BETWEEN } / { Sum Of Squares WITHIN / df-WITHIN } => This expression of the F-Statistic I conceptually and intuitively understand.

However, there are some other Variations for the F -Statistic Formula

F -Statistic = { ( SSR-Restricted - SSR-UNRestricted ) / No of Restrictions } / (SSR-UNRestricted ) /(N-k-1) which again I understand the conceptually and intuitively.

Also,

F -Statistic = { (R-UNRestricted ^2 - R-Restricted ^ 2 ) /q } / ( 1- R-UNRestricted ^2 ) / (N-k-1)

How does ( SSR-Restricted - SSR-UNRestricted ) translate to (R-UNRestricted ^2 - R-Restricted ^ 2 ) given that in general, R^2 = { 1 - SSR/ (SSR + SSExplained)

@David Harper CFA FRM had indicated in a thread that -" The general form of the F-statistic is F[numerator df, denominator df] = (ESS/df)/(RSS/df) "

F -Statistic is also expressed as = {Sum Of Squares BETWEEN / df-BETWEEN } / { Sum Of Squares WITHIN / df-WITHIN } => This expression of the F-Statistic I conceptually and intuitively understand.

However, there are some other Variations for the F -Statistic Formula

F -Statistic = { ( SSR-Restricted - SSR-UNRestricted ) / No of Restrictions } / (SSR-UNRestricted ) /(N-k-1) which again I understand the conceptually and intuitively.

Also,

F -Statistic = { (R-UNRestricted ^2 - R-Restricted ^ 2 ) /q } / ( 1- R-UNRestricted ^2 ) / (N-k-1)

How does ( SSR-Restricted - SSR-UNRestricted ) translate to (R-UNRestricted ^2 - R-Restricted ^ 2 ) given that in general, R^2 = { 1 - SSR/ (SSR + SSExplained)

")