You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Expected Shortfall

- Thread starter bball8530

- Start date

hi,

probability of 2 defaults=P(D)*P(D)=.02^2=.0004 =.04%(2C2(.02)^2*(.98)^0)

probability of 1 defaults=P(ND)*P(D) or P(D)*P(ND) =(1-.02)*.02+(1-.02)*.02=2*.0196 =.0392=3.92%(2C1(.02)^1*(.98)^1)

probability of 0 defaults=1-[probability of 2 defaults+probability of 1 defaults]=1-(3.92%+.04%)=1-3.96%=96.04%(2C0(.02)^0*(.98)^2)

thanks

probability of 2 defaults=P(D)*P(D)=.02^2=.0004 =.04%(2C2(.02)^2*(.98)^0)

probability of 1 defaults=P(ND)*P(D) or P(D)*P(ND) =(1-.02)*.02+(1-.02)*.02=2*.0196 =.0392=3.92%(2C1(.02)^1*(.98)^1)

probability of 0 defaults=1-[probability of 2 defaults+probability of 1 defaults]=1-(3.92%+.04%)=1-3.96%=96.04%(2C0(.02)^0*(.98)^2)

thanks

hi,

please check for dome typo/error in the Q solution. verify it with david. definitely sure its 96.04% instead of 1.04%

thanks

please check for dome typo/error in the Q solution. verify it with david. definitely sure its 96.04% instead of 1.04%

thanks

I believe 1.04% is correct as the sum of the three probabilities needs to equal 5% as we are dividing each by 5% to get the weighted average in the 5% tail. I'm just wondering how 1.04% is derived. The 3.92% and .04% make sense. If you take 5%- 3.92%-.04% = 1.04% but I feel there's a different method/formula to come up with the 1.04%...

For 5% tail than it should be 96.04-95=1.04% probability of no default in the tail region and since u need to find the no default possibility for the tail region only , hence its appropriate to consider 1.04%.

thanks

thanks

Yes, thanks bball8530 and ShaktiRathore, I agree with all above (I tagged the exhibit for revision because it would be a clearer exhibit to show the final calc in the XLS)

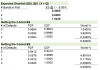

The other two PDFs (which I'd prefer were labelled PMFs, as this is a discrete distribution) of 3.92% (default = 1) and 0.040% (default = 2) are included, in full because they are fully within the 5.0% tail.

In a discrete distribution, it is a matter of identifying the PMF that "straddles" the quantile. At defaults = 0, the PMF = 96.04% overwhelms most of the distribution and "spills a bit into" the 5% tail. So, i think of it as "chopping off" the 1.04% that falls into the 5% tail, per Shakti's 96.05% - (1 - 5%) = 1.04%.

If instead the ES here were 10% instead of 5%; i.e., 90% ES then all rows the same except the first is now 96.05% - (1 - 10%) = 6.04%, with resulting reduction of ES from 0.8 to 0.4 (since we just expanded the tail to include an piece consisting entirely of zero, so the weighted average cuts in half). Thanks,

The other two PDFs (which I'd prefer were labelled PMFs, as this is a discrete distribution) of 3.92% (default = 1) and 0.040% (default = 2) are included, in full because they are fully within the 5.0% tail.

In a discrete distribution, it is a matter of identifying the PMF that "straddles" the quantile. At defaults = 0, the PMF = 96.04% overwhelms most of the distribution and "spills a bit into" the 5% tail. So, i think of it as "chopping off" the 1.04% that falls into the 5% tail, per Shakti's 96.05% - (1 - 5%) = 1.04%.

If instead the ES here were 10% instead of 5%; i.e., 90% ES then all rows the same except the first is now 96.05% - (1 - 10%) = 6.04%, with resulting reduction of ES from 0.8 to 0.4 (since we just expanded the tail to include an piece consisting entirely of zero, so the weighted average cuts in half). Thanks,

afterworkguinness

Active Member

Thanks for clarifying how to arrive at the 1.04%; that had me stumped.

I'm curious though, isn't ES supposed to be equally weighted for historic simulation ?

I'm curious though, isn't ES supposed to be equally weighted for historic simulation ?

Last edited:

I'm curious though, isn't ES supposed to be equally weighted for historic simulation ?

I guess the short answer is, this is not historical simulation.

The slightly longer answer:

If you would conduct a monte-carlo simulation with the above probabilities and look at the worst 5% of your simulation runs, you would find 0,04% of your runs have 2 defaults, 3,92% have 1 default. Now you are left with 96,04% with 0 defaults, which are all equally bad. So to get to your worst 5% you have to fill them up with 1,04% of runs with 0 defaults. If you weight these monte-carlo runs all equally, you again arrive at the above result.

afterworkguinness

Active Member

Thanks for your reply ami44. Why wouldn't this method be classified as a historical simulation? We are observing empirical returns in the tail...

Sorry, i was unclear:

Calculatimg the ES from the probabilities, like it was done in the solution to the original exercise is not historical simulation. Because you calculate from PDs and assumed distributions and not from empirical returns.

But if you conduct a Monte Carlo Simulation, as I suggested as a thought experiment, than you have (simulated) empirical returns and then you weight them equally.

The resulting value for ES is of course the same.

Was that clearer?

Calculatimg the ES from the probabilities, like it was done in the solution to the original exercise is not historical simulation. Because you calculate from PDs and assumed distributions and not from empirical returns.

But if you conduct a Monte Carlo Simulation, as I suggested as a thought experiment, than you have (simulated) empirical returns and then you weight them equally.

The resulting value for ES is of course the same.

Was that clearer?

afterworkguinness

Active Member

Thanks ami44

hi,

probability of 2 defaults=P(D)*P(D)=.02^2=.0004 =.04%(2C2(.02)^2*(.98)^0)

probability of 1 defaults=P(ND)*P(D) or P(D)*P(ND) =(1-.02)*.02+(1-.02)*.02=2*.0196 =.0392=3.92%(2C1(.02)^1*(.98)^1)

probability of 0 defaults=1-[probability of 2 defaults+probability of 1 defaults]=1-(3.92%+.04%)=1-3.96%=96.04%(2C0(.02)^0*(.98)^2)

thanks

probability of 1 defaults=P(ND)*P(D) or P(D)*P(ND) =(1-.02)*.02+(1-.02)*.02=2*.0196 =.0392=3.92%(2C1(.02)^1*(.98)^1)

If (1-.02)*.02 is the probability of 1 default per probability of 1 defaults=P(ND)*P(D), why are we multiplying by 2?

@bpdulog Here is the xls @ http://trtl.bz/es-three-bonds e.g. ,

0.0576 is a straight-up binomial PDF: Pr[X = 1 default | n = 3 bonds, p = 2%] = 2%*98%*98%*C(3,1) = 2%*98%*98%*3, because there are three combinations of one default in a 3-bond portfolio: SSD, SDS, DSS (where S=survive and D=default). Thanks,

0.0576 is a straight-up binomial PDF: Pr[X = 1 default | n = 3 bonds, p = 2%] = 2%*98%*98%*C(3,1) = 2%*98%*98%*3, because there are three combinations of one default in a 3-bond portfolio: SSD, SDS, DSS (where S=survive and D=default). Thanks,

Similar threads

- Replies

- 1

- Views

- 240

- Replies

- 0

- Views

- 199

- Replies

- 0

- Views

- 231

- Replies

- 0

- Views

- 125