Hi @jack11961 But they are both saying (correctly) the same thing:

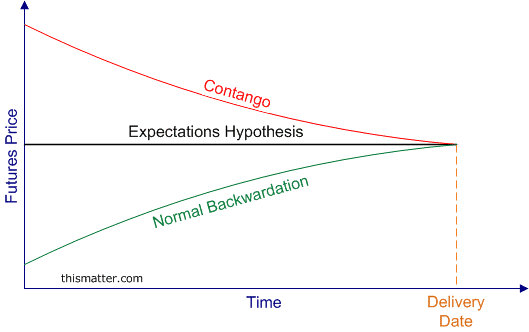

As time marches forward (moving forward in time), under normal backwardation (assuming constant or at least non-decreasing spot) the futures price is increasing; or equivalently

By definition of normal backwardation the futures price is an decreasing function of maturity; i.e., S(0) > F(+1 month) > F(+2 months)

This site uses cookies to help personalise content, tailor your experience and to keep you logged in if you register.

By continuing to use this site, you are consenting to our use of cookies.