Learning objectives: Examine how the clearing of over-the-counter transactions through central counterparties has affected risks in the financial system. Assess whether central clearing has enhanced financial stability and reduced systemic risk. Describe the transformation of counterparty risk into liquidity risk. Explain how liquidity of clearing members and liquidity resources of CCPs affect risk management and financial stability. Compare and assess methods a CCP can use to help recover capital when a member defaults or when a liquidity crisis occurs.

Questions:

804.1. In the typical central counterparty (CCP) loss waterfall, if a clearing member defaults then the first layer of protection is the defaulting member's own initial margin. However, if this initial margin contribution is insufficient, which of the following is the next source of funds in the loss waterfall?

a. The general default fund

b. The CCP's "skin in the game"

c. The initial margin of other, non-defaulting members

d. The default fund contribution of the defaulting member

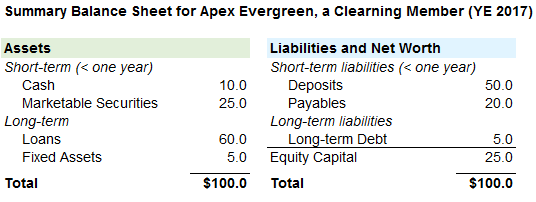

804.2. Apex Evergreen is a clearing member with the following summary balance sheet:

Which of the following statements is TRUE?

a. Apex is insolvent

b. Apex is in default

c. Apex is not liquid (aka, illiquid)

d. Apex has a leverage ratio of 20.0

804.3. Rama Cont writes that "the introduction of central clearing in OTC markets has been effective in reducing counterparty exposures across clearing members. But, rather than removing counterparty risk, central clearing transforms it [...]". According to Cont, each of the following statements is true EXCEPT which is false?

a. The transfer of initial margin and variation margin from the clearing member to the CCP reduces the firm's solvency but is neutral with respect to the member's liquidity

b. Although market risk depends on the net position for a long-short portfolio, the liquidation cost is proportional to the gross notional size

c. Margin requirements should include a liquidity charge that is higher for portfolios with (i) positions whose sizes are large relative to market depth and/or (ii) positions in less liquid instruments

d. If the liquidation horizon increases linearly with the notional size (N), and the notional size of a position increases by a factor of four (4), then value at risk (VaR) or expected shortfall (ES) increase by a factor of four, but the liquidation costs is likely to increase by a factor of eight (8)

Answers here:

Questions:

804.1. In the typical central counterparty (CCP) loss waterfall, if a clearing member defaults then the first layer of protection is the defaulting member's own initial margin. However, if this initial margin contribution is insufficient, which of the following is the next source of funds in the loss waterfall?

a. The general default fund

b. The CCP's "skin in the game"

c. The initial margin of other, non-defaulting members

d. The default fund contribution of the defaulting member

804.2. Apex Evergreen is a clearing member with the following summary balance sheet:

Which of the following statements is TRUE?

a. Apex is insolvent

b. Apex is in default

c. Apex is not liquid (aka, illiquid)

d. Apex has a leverage ratio of 20.0

804.3. Rama Cont writes that "the introduction of central clearing in OTC markets has been effective in reducing counterparty exposures across clearing members. But, rather than removing counterparty risk, central clearing transforms it [...]". According to Cont, each of the following statements is true EXCEPT which is false?

a. The transfer of initial margin and variation margin from the clearing member to the CCP reduces the firm's solvency but is neutral with respect to the member's liquidity

b. Although market risk depends on the net position for a long-short portfolio, the liquidation cost is proportional to the gross notional size

c. Margin requirements should include a liquidity charge that is higher for portfolios with (i) positions whose sizes are large relative to market depth and/or (ii) positions in less liquid instruments

d. If the liquidation horizon increases linearly with the notional size (N), and the notional size of a position increases by a factor of four (4), then value at risk (VaR) or expected shortfall (ES) increase by a factor of four, but the liquidation costs is likely to increase by a factor of eight (8)

Answers here: