Learning objectives: Explain the impact of changing assumptions used in calculating economic capital, including choosing a time horizon, measuring default probability, and choosing a confidence level. Calculate the hurdle rate and apply this rate in making business decisions using RAROC. Compute the adjusted RAROC for a project to determine its viability. Explain challenges in modeling diversification benefits, including aggregating a firm’s risk capital and allocating economic capital to different business lines. Explain best practices in implementing a RAROC approach.

Questions:

607.1. Assume a bank's $2.0 billion corporate loan portfolio offers a return of 6.0% per annum. The expected loss on the portfolio is estimated to be 1.5% per annum; i.e., $30 million. The portfolio is funded by $2.0 billion in retail deposits with a transfer-priced interest rate charge of 2.00%. The bank (the lender) has a direct operating cost of $16.0 million per annum and an effective tax rate of 25.0%. Risk analysis of the unexpected losses associated with the portfolio tell us we need to set aside economic capital of $200.0 million against the portfolio; i.e., 10.0% of the loan amount. The bank's economic capital must be invested in risk-free securities and, unfortunately in the regime of ultra low interest rates, the risk-free rate on government securities is only 1.0%.

Although the loan portfolio's risk-adjusted return on capital (RAROC) is positive and seemingly high, the bank wants to adjust the traditional RAROC calculation to obtain a RARO measures that takes into account the systemic riskiness of the expected returns. If the risk-free rate is 1.0% (as above), and the expected rate of return on the market portfolio is 8.0% such that the equity risk premium is 7.0%, and the beta of the firm's equity is 1.60, which of the following is the correct adjusted RAROC and is the project advisable?

a. RAROC is 6.25% but no, the project is bad because ARAROC is below the risk-free rate

b. RAROC is 8.00% but no, the project is bad because ARAROC is below the risk-free rate

c. RAROC is 9.80% and yes, the project is good because ARAROC is above the risk-free rate

d. RAROC is 13.50% and yes, the project is good because ARAROC is above the risk-free rate

607.2. Consider a business unit (BU) which consists of two activities, X and Y, for which the firm's risk staff has calculated three different measures of risk capital:

Please note:

a. Given that the risk capital for the business unit is $120.0 (as shown), the implied correlation between activities must be zero

b. Fully diversified capital ($56 for X and $64 for Y) should be used for assessing the solvency of the firm and minimum risk pricing

c. Incremental capital (aka, Crouhy's marginal risk capital; $40 for X and $40 for Y) should be used for active portfolio management or business mix decisions,

d. Stand-alone capital ($70 for X and $80 for Y) should be used for incentive compensation; and fully-diversified capital ($56 for X and $64 for Y) can be used to assess the extra performance generated by the diversification effects, such that performance measurement involve both stand-alone and fully-diversified perspectives

607.3. According to Crouhy, Galai and Mark, best practice in the implementation of a RAROC system should include each of the following elements EXCEPT which is incorrect?

a. Given the strategic nature of the decisions steered by a RAROC system, the marching orders must come from the top management of the firm; specifically, the CEO and his or her executive team should sponsor the implementation of a RAROC system and should be active in its diffusion

b. In order to preserve the integrity and transparency of the RAROC system, there should be a an exclusively quantitative decision rule for activities: if the ex ante RAROC does not exceed the firm's hurdle rate (if the RAROC return is "low"), the firm should exit the activity

c. The value at risk (VaR) methodologies for measuring market risk and credit risk that underpin RAROC calculations are "generally well accepted" by business units (although this is not yet true for operational risk); in practice, disagreements concern the setting of the parameters that feed into these models which determine the size of economic capital

d. Balance sheet requests from the business units, such as economic capital, leverage ratio, liquidity ratios, and risk-weighted assets, should be channeled to the RAROC group every quarter; limits are then set for economic capital, leverage ratio, liquidity ratios, and risk-weighted assets

Answers here:

Questions:

607.1. Assume a bank's $2.0 billion corporate loan portfolio offers a return of 6.0% per annum. The expected loss on the portfolio is estimated to be 1.5% per annum; i.e., $30 million. The portfolio is funded by $2.0 billion in retail deposits with a transfer-priced interest rate charge of 2.00%. The bank (the lender) has a direct operating cost of $16.0 million per annum and an effective tax rate of 25.0%. Risk analysis of the unexpected losses associated with the portfolio tell us we need to set aside economic capital of $200.0 million against the portfolio; i.e., 10.0% of the loan amount. The bank's economic capital must be invested in risk-free securities and, unfortunately in the regime of ultra low interest rates, the risk-free rate on government securities is only 1.0%.

Although the loan portfolio's risk-adjusted return on capital (RAROC) is positive and seemingly high, the bank wants to adjust the traditional RAROC calculation to obtain a RARO measures that takes into account the systemic riskiness of the expected returns. If the risk-free rate is 1.0% (as above), and the expected rate of return on the market portfolio is 8.0% such that the equity risk premium is 7.0%, and the beta of the firm's equity is 1.60, which of the following is the correct adjusted RAROC and is the project advisable?

a. RAROC is 6.25% but no, the project is bad because ARAROC is below the risk-free rate

b. RAROC is 8.00% but no, the project is bad because ARAROC is below the risk-free rate

c. RAROC is 9.80% and yes, the project is good because ARAROC is above the risk-free rate

d. RAROC is 13.50% and yes, the project is good because ARAROC is above the risk-free rate

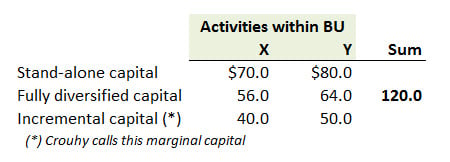

607.2. Consider a business unit (BU) which consists of two activities, X and Y, for which the firm's risk staff has calculated three different measures of risk capital:

Please note:

- Stand-alone capital is the capital used by an activity taken independently of the other activities in the same business unit; ie, risk capital calculated without any diversification benefits. Here the stand-alone capital for X is $ 70 and for Y it is $ 80.

- Fully diversified capital is the capital attributed to each activity X and Y, taking into account all diversification benefits from combining them under the same leadership. Here the overall portfolio effect is $30 = $70 + 80 - 120. The firm's analysts allocated the portfolio effect pro rata with the stand-alone risk capital: $30 × 70/150 = $14 for X and $30 × 80/150 = $16 for Y, so that the fully diversified risk capital becomes $56 for X and $64 for Y.

- Incremental capital (which is called marginal capital by Crouhy) is the additional capital required by an incremental deal, activity, or business. It takes into account the full benefit of diversification. Here the marginal risk capital for X (assuming that Y already exists) is $40 = $120 - 80, and the marginal risk capital for Y (assuming that X already exists) is $50 = $120 - 70. The summation of the marginal risk capital, $90 in this example, is less than the full risk capital of the BU.

a. Given that the risk capital for the business unit is $120.0 (as shown), the implied correlation between activities must be zero

b. Fully diversified capital ($56 for X and $64 for Y) should be used for assessing the solvency of the firm and minimum risk pricing

c. Incremental capital (aka, Crouhy's marginal risk capital; $40 for X and $40 for Y) should be used for active portfolio management or business mix decisions,

d. Stand-alone capital ($70 for X and $80 for Y) should be used for incentive compensation; and fully-diversified capital ($56 for X and $64 for Y) can be used to assess the extra performance generated by the diversification effects, such that performance measurement involve both stand-alone and fully-diversified perspectives

607.3. According to Crouhy, Galai and Mark, best practice in the implementation of a RAROC system should include each of the following elements EXCEPT which is incorrect?

a. Given the strategic nature of the decisions steered by a RAROC system, the marching orders must come from the top management of the firm; specifically, the CEO and his or her executive team should sponsor the implementation of a RAROC system and should be active in its diffusion

b. In order to preserve the integrity and transparency of the RAROC system, there should be a an exclusively quantitative decision rule for activities: if the ex ante RAROC does not exceed the firm's hurdle rate (if the RAROC return is "low"), the firm should exit the activity

c. The value at risk (VaR) methodologies for measuring market risk and credit risk that underpin RAROC calculations are "generally well accepted" by business units (although this is not yet true for operational risk); in practice, disagreements concern the setting of the parameters that feed into these models which determine the size of economic capital

d. Balance sheet requests from the business units, such as economic capital, leverage ratio, liquidity ratios, and risk-weighted assets, should be channeled to the RAROC group every quarter; limits are then set for economic capital, leverage ratio, liquidity ratios, and risk-weighted assets

Answers here:

")