Learning objective: Describe the method of mapping forwards, forward rate agreements, interest rate swaps, and options.

Questions:

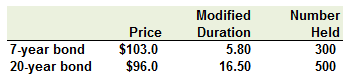

717.1. A portfolio manager evaluates the risk of the following two-bond portfolio:

We assume that specific risk is negligible and that the volatility of changes in market yields is 50 basis points. Under these conditions, which is nearest to the volatility of the portfolio value? (note: variation on Jorion's EOC question 11.8) (Philippe Jorion, Value-at-Risk: The New Benchmark for Managing Financial Risk, 3rd Edition (New York: McGraw Hill, 2006))

a. $1,065

b. $3,230

c. $4,856

d. $9,700

717.2. In regard to value at risk (VaR) mapping, each of the following statements is true EXCEPT which is false?

a. A forward currency position has three major risk factors: the spot price and two interest rates

b. A consumption commodity forward contract is more likely to be directly mapped the commodity's volatile forward price than an investment commodity forward

c. A forward rate agreement can be mapped to two risk factors: a long position in a zero-coupon bond (or bill) plus a short position in a zero-coupon bond (or bill)

d. Because an interest rate swap is a bilateral contract, it cannot be effectively mapped to primitive risk factors and simulation must be used to compute a diversified VaR

717.3. In January, Stacy the Risk Analyst has mapped a large and LONG position in call options with the following profile:

a. She adds the risk-free interest rate (rho) as a risk factor because expiration is now virtually certain

b. She adds gamma as a risk factor because the first-order linear approximation has become insufficient

c. She adds vega as a risk factor which was omitted at long maturities but is more relevant at short maturities

d. She adds delta as a risk factor which had a low profile at longer terms but, for ATM options, becomes more relevant as maturity approaches

Answers here:

Questions:

717.1. A portfolio manager evaluates the risk of the following two-bond portfolio:

We assume that specific risk is negligible and that the volatility of changes in market yields is 50 basis points. Under these conditions, which is nearest to the volatility of the portfolio value? (note: variation on Jorion's EOC question 11.8) (Philippe Jorion, Value-at-Risk: The New Benchmark for Managing Financial Risk, 3rd Edition (New York: McGraw Hill, 2006))

a. $1,065

b. $3,230

c. $4,856

d. $9,700

717.2. In regard to value at risk (VaR) mapping, each of the following statements is true EXCEPT which is false?

a. A forward currency position has three major risk factors: the spot price and two interest rates

b. A consumption commodity forward contract is more likely to be directly mapped the commodity's volatile forward price than an investment commodity forward

c. A forward rate agreement can be mapped to two risk factors: a long position in a zero-coupon bond (or bill) plus a short position in a zero-coupon bond (or bill)

d. Because an interest rate swap is a bilateral contract, it cannot be effectively mapped to primitive risk factors and simulation must be used to compute a diversified VaR

717.3. In January, Stacy the Risk Analyst has mapped a large and LONG position in call options with the following profile:

- Ratio of spot price to strike price, S/K: Approximately 1.0

- Implied volatility: ~ 23.0% per annum

- Time to expiration: Six months (mature in July)

- Risk-free rate assumption: 1.50%

a. She adds the risk-free interest rate (rho) as a risk factor because expiration is now virtually certain

b. She adds gamma as a risk factor because the first-order linear approximation has become insufficient

c. She adds vega as a risk factor which was omitted at long maturities but is more relevant at short maturities

d. She adds delta as a risk factor which had a low profile at longer terms but, for ATM options, becomes more relevant as maturity approaches

Answers here:

Last edited: