fullofquestions

New Member

QUESTION

You want to implement a portfolio insurance strategy using index futures designed to protect the value

of a portfolio of stocks not paying any dividends. Assuming the value of your stock portfolio decreases,

which strategy would you implement to protect your portfolio?

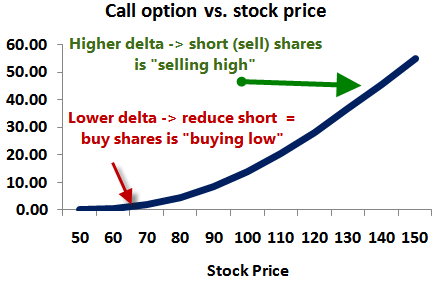

a. Buy an amount of index futures equivalent to the change in the call delta x original portfolio value.

b. Sell an amount of index futures equivalent to the change in the call delta x original portfolio value.

c. Buy an amount of index futures equivalent to the change in the put delta x original portfolio value.

d. Sell an amount of index futures equivalent to the change in the put delta x original portfolio value.

Answer: d

a. Incorrect. For portfolio insurance strategy to work, index futures should be sold in an amount

corresponding to the change in the put delta x original portfolio value.

b. Incorrect. For portfolio insurance strategy to work, index futures should be sold in an amount

corresponding to the change in the put delta x original portfolio value.

c. Incorrect. For portfolio insurance strategy to work, index futures should be sold in an amount

corresponding to the change in the put delta x original portfolio value.

d. Correct. Portfolio insurance strategy is accomplished by selling index futures contracts in an amount

equivalent to the proportion of the portfolio dictated by the delta of the required put option. When a

decrease in the value of the underlying portfolio occurs, the amount of additional index futures sold

corresponds to the change in the put delta x original portfolio value.

Where in Hull sixth edition is this? I looked in the 'Use of Index Futures' section (p366) and did not find anything. Can someone point me to the page or give me an explanation? Clearly you have to sell to hedge the long exposure (the fact that you are long is barely obvious here), but I really don't know how the call vs. put delta provide a different answer. Any thoughts?

You want to implement a portfolio insurance strategy using index futures designed to protect the value

of a portfolio of stocks not paying any dividends. Assuming the value of your stock portfolio decreases,

which strategy would you implement to protect your portfolio?

a. Buy an amount of index futures equivalent to the change in the call delta x original portfolio value.

b. Sell an amount of index futures equivalent to the change in the call delta x original portfolio value.

c. Buy an amount of index futures equivalent to the change in the put delta x original portfolio value.

d. Sell an amount of index futures equivalent to the change in the put delta x original portfolio value.

Answer: d

a. Incorrect. For portfolio insurance strategy to work, index futures should be sold in an amount

corresponding to the change in the put delta x original portfolio value.

b. Incorrect. For portfolio insurance strategy to work, index futures should be sold in an amount

corresponding to the change in the put delta x original portfolio value.

c. Incorrect. For portfolio insurance strategy to work, index futures should be sold in an amount

corresponding to the change in the put delta x original portfolio value.

d. Correct. Portfolio insurance strategy is accomplished by selling index futures contracts in an amount

equivalent to the proportion of the portfolio dictated by the delta of the required put option. When a

decrease in the value of the underlying portfolio occurs, the amount of additional index futures sold

corresponds to the change in the put delta x original portfolio value.

Where in Hull sixth edition is this? I looked in the 'Use of Index Futures' section (p366) and did not find anything. Can someone point me to the page or give me an explanation? Clearly you have to sell to hedge the long exposure (the fact that you are long is barely obvious here), but I really don't know how the call vs. put delta provide a different answer. Any thoughts?

")